Will mortgage rates revive India’s residential segment?

The government and the central bank have been introducing several reforms to take care of the muted consumer sentiment. What impact, if any does that have on the home-buyer sentiment in regards to residential purchases?

The residential sector has been resilient through the disruptions of RERA (Real estate Regulatory Authority Act), GST (Goods & Services Tax) and demonetisation. The growth momentum continued in previous years with residential sales recording a 6% y-o-y growth across the top seven cities in India, even though the overall economic growth remained subdued. However, 2020 is likely to be turbulent for the sector due to the recent health crisis. While the first two months of the quarter witnessed sales across segments, the nation-wide lockdown disrupted this momentum in the month of March. The impact of the pandemic manifested in the form of reduced walk-ins as home-buyers began to delay their decisions amidst uncertainty over jobs and salary cuts. The result was a 29% decline in sales across cities in Q1 2020 as compared to Q1 2019.

To revive the real estate sector, the government has introduced several relief measures, including the extension of moratorium periods and project completion dates, and special liquidity schemes for NBFCs and HFCs. However, considering the sector contributes around 8% to our GDP and is the second-largest employer in the country, sector-specific reforms, such as restructuring of loans, which could have steepened the growth curve, are missing.

The Reserve Bank of India (RBI) has also made efforts to uplift consumer demand through its monetary policies. The RBI has followed a series of rate cuts since February 2019 to arrest falling consumption trends. The repo rate currently stands at 4%, which is lower than the rate observed during the Global Financial Crisis of 2008-09 (4.75%). These continuous corrections in policy rates reflect the seriousness of the current downturn.

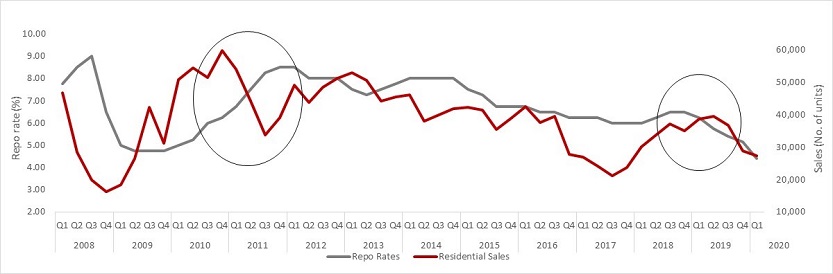

Figure 1 traces how changes in policy rates impact residential sales. While the reduction in policy rates has exhibited an inverse relationship with residential sales in the past, it has weakened over the last 2-3 years. The positive impact of rate cuts was much stronger in the subsequent quarters of 2011 than it has been after 2015. An interesting pattern to note here is the dip in residential sales during 2017, which was due to demonetisation in Q4 2016. Besides, reforms such as GST and RERA also disrupted the sector for a while. Evidently, the policy rates were not the only factors that determined house purchases. Similarly, in 2019, the consecutive rate cuts since the beginning of the year seem to have little impact on residential sales, which dipped simultaneously.

Figure 1: Repo rates vs Residential Sales

Source: RBI, JLL Research and REIS

While the banks have been passing on the reduction in policy rates to end-consumers through mortgage rates, it hasn’t been enough to drive fence-sitters to effect purchases. Clearly, a reduction in mortgage rates is necessary when determining home purchases since it is the cost of funds, but it is not sufficient to drive sales. A home-buyer takes into account other economic conditions such as economic growth and their income stability. With the current muted consumer sentiment and uncertainty around job security and income stability, what is probably required is a policy that improves the overall economic outlook and gives relief to the staggering sector.